Stable long-term demand for funding despite new COVID-19 outbreaks

Authored by Leela Vosko

Global Sector Outlook

As we approach the end of 2021, we have seen how a majority of the world’s governments and regulatory institutions have learned to manage outbreaks and new strains of COVID-19, such as the Delta and Omicron variants. As more countries realize that zero tolerance policies come with tradeoffs, the economic impact of COVID-19 on individual countries and global trade is likely to become less severe as time passes, notwithstanding the supply chain imbalances that have dominated the news. As a result, economic disruptions are expected to be smaller in the coming year than those at the beginning of the pandemic.

As financial markets have encountered far less disruption in the recent period, so have the operations of our portfolio of Micro and SME Finance Institutions. Most of whom have learned to anticipate future surges of COVID-19 cases and focused on prudently managing their liquidity and operations to make it through short-term dislocations.

During Q3 2021, despite a larger surge in COVID-19 cases in some countries, MicroVest received and granted just two new forbearances, compared to 12 at the onset of the pandemic in Q2 2020. As an illustrative example, despite the Delta Wave, one of our portfolio companies in Myanmar—perhaps our most challenged market currently—was able to reduce its loan balance by 50% in Q3 based on prudent liquidity management. The fact that this portfolio company was able to manage its own borrowing base to build liquidity and pay down balances to international lenders like MicroVest is remarkable given the challenging circumstances in the country between COVID-19 and civil strife. Nevertheless, we are cautious on our outlook for our Myanmar exposure given the evolving situation in the country.

While there are numerous examples that showcase that our portfolio companies are bouncing back, we are not underestimating the lingering impact of the pandemic on our markets. Early on during COVID-19, vaccination rates provided a useful barometer of whether a country’s economy could safely reopen. While this was largely true in developed countries, it did not bode well for emerging and frontier markets for two reasons. First, the average vaccination rate among emerging and frontier countries, which includes fully and partially vaccinated individuals, is only 27.9%.1 Some countries are dramatically below even this figure. Second, the vaccines developed up until this point have demonstrated decreased efficacy against the Delta variant of COVID-19, which necessitates booster shots for some populations. This means that future mutations of the virus may further decrease the efficacy of the existing vaccines, which would extend the time horizon for the pandemic. MicroVest’s borrowers will likely continue to experience periodic spikes in non-preforming loans as countries reimplement measures to control new outbreaks, but we expect the impact will be less severe compared to the initial effects that began in March 2020.

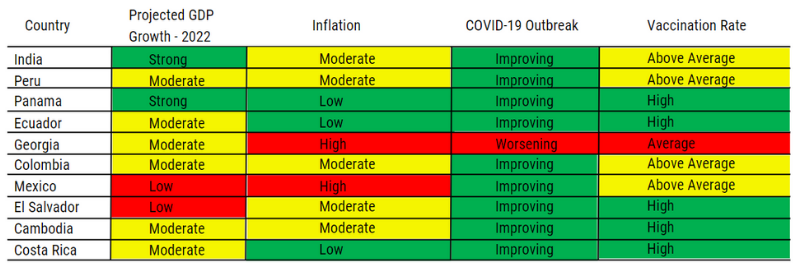

The table below captures our Risk Team’s assessment as of November 2021, of the top 10 countries represented in our portfolio by assets invested. In addition to analyzing the trend of COVID-19 outbreaks and our views regarding the widespread availability of a vaccine, we also consider whether the economy is recovering and the quality of government fiscal policy measures to stimulate aggregate demand and provide relief to vulnerable members of society.

Demand Outlook

Since March 2020, our portfolio of Micro and SME Finance Institutions steadily built up their liquidity. This is a result of 1) prudence on their behalf; and 2) a decrease in demand from local borrowers due to economic restrictions and government support measures in some countries. As vaccination rates increased and restrictions were gradually lifted, our portfolio companies planned for significant growth in the second half of this year. MicroVest benefitted from these plans and originated a record level of transaction volume during the second quarter. However, beginning in late June, those growth plans faced temporary setbacks as the Delta variant spread and outpaced vaccination rates. Several markets reimposed targeted restrictions in July/August to curb the spread of Delta. While the impact of this COVID-19 wave was less financially disruptive than the initial surge in 2020, our portfolio companies’ operations were affected in two primary ways:

By the end of the third quarter, the delta wave had run its course, cases rapidly declined, and governments loosed or removed restrictions in most countries. The responsiveness of our Micro and SME Finance Institutions improved, loan processes resumed, and MicroVest began executing planned transactions with strong borrowers. Despite short-term ebbs and flows of demand due to virus surges, the annual financing need from our portfolio remains robust. Asset growth of our portfolio is still greater than 10%, despite pandemic effects. We consider that long-term demand to be stable regardless of new COVID-19 outbreaks, as our investee portfolio companies consistently need funding to meet demand for loans in their communities.

Yield Outlook

MicroVest is seeing modest pressure on yields, stemming from a flight to quality of Micro and SME Finance Institutions combined with an extended period of low interest rates and significant liquidity provided by central banks. While MicroVest’s portfolios will generate gross yields close to target, we are seeing some new transactions renew at lower yields. The extent to which this continues will be a function of demand dynamics mentioned above, combined with interest rate and inflation trends that are a subject debate in global finance. Central banks may be forced to choose between raising benchmark rates to contain inflation or leaving rates at low levels, which would risk inflation continuing to run above benchmark levels. For example, the topic of raising rates has gained additional support in recent months in both the U.S. Federal Reserve and the Bank of England. During the last month, a number of central banks in developing economies have raised rates, including Mexico, Colombia, Brazil, and Russia. A rising global interest rate environment should benefit MicroVest’s gross yields in the long run but may put stress on portfolio quality metrics if combined with inflation that impacts local economies in meaningful ways.

Overall Outlook

Despite risks on the horizon, we continue to see strong collection trends and growing loan origination now that the Delta wave has subsided in most markets. We believe that future growth will remain resilient given the persistence of significant financing gaps, though we remain cautious as increasing vaccination rates in emerging markets will be the best buffer against volatility and make them more resilient against additional waves of COVID-19.

1As of November 2021. https://ourworldindata.org/covid-vaccinations

DISCLOSURE INFORMATION

The information contained in this communication has been provided by MicroVest Capital Management, LLC (“MicroVest”) and no representation or warranty, expressed or implied is made by MicroVest as to the accuracy or completeness of the information contained herein. Any forward-looking statements contained herein with respect to MicroVest’s plans and strategies, anticipated capital investments, changes in market conditions, financial projections or any other matters that are not historical facts, are only predictions and estimates regarding future events and circumstances. Market conditions and MicroVest’s actual results may differ materially from the market conditions and results discussed in these statements.